![]()

Package runstats provides methods for fast computation

of running sample statistics for time series. The methods utilize

Convolution Theorem to compute convolutions via Fast Fourier Transform

(FFT). Implemented running statistics include:

Package website is located here.

# devtools::install_github("martakarass/runstats")

install.packages("runstats")library(runstats)

## Example: running correlation

x0 <- sin(seq(0, 2 * pi * 5, length.out = 1000))

x <- x0 + rnorm(1000, sd = 0.1)

pattern <- x0[1:100]

out1 <- RunningCor(x, pattern)

out2 <- RunningCor(x, pattern, circular = TRUE)

## Example: running mean

x <- cumsum(rnorm(1000))

out1 <- RunningMean(x, W = 100)

out2 <- RunningMean(x, W = 100, circular = TRUE)To better explain the details of running statistics, package’s

function runstats.demo(func.name) allows to visualize how

the output of each running statistics method is generated. To run the

demo, use func.name being one of the methods’ names:

"RunningMean","RunningSd","RunningVar","RunningCov","RunningCor","RunningL2Norm".## Example: demo for running correlation method

runstats.demo("RunningCor")

## Example: demo for running mean method

runstats.demo("RunningMean")

We use rbenchmark to measure elapsed time of

RunningCov execution, for different lengths of time-series

x and fixed length of the shorter pattern

y.

library(rbenchmark)

set.seed (20181010)

x.N.seq <- 10^(3:7)

x.list <- lapply(x.N.seq, function(N) runif(N))

y <- runif(100)

## Benchmark execution time of RunningCov

out.df <- data.frame()

for (x.tmp in x.list){

out.df.tmp <- benchmark("runstats" = runstats::RunningCov(x.tmp, y),

replications = 10,

columns = c("test", "replications", "elapsed",

"relative", "user.self", "sys.self"))

out.df.tmp$x_length <- length(x.tmp)

out.df.tmp$pattern_length <- length(y)

out.df <- rbind(out.df, out.df.tmp)

}knitr::kable(out.df)| test | replications | elapsed | relative | user.self | sys.self | x_length | pattern_length |

|---|---|---|---|---|---|---|---|

| runstats | 10 | 0.005 | 1 | 0.004 | 0.001 | 1000 | 100 |

| runstats | 10 | 0.023 | 1 | 0.018 | 0.004 | 10000 | 100 |

| runstats | 10 | 0.194 | 1 | 0.158 | 0.037 | 100000 | 100 |

| runstats | 10 | 1.791 | 1 | 1.656 | 0.125 | 1000000 | 100 |

| runstats | 10 | 20.234 | 1 | 17.660 | 2.514 | 10000000 | 100 |

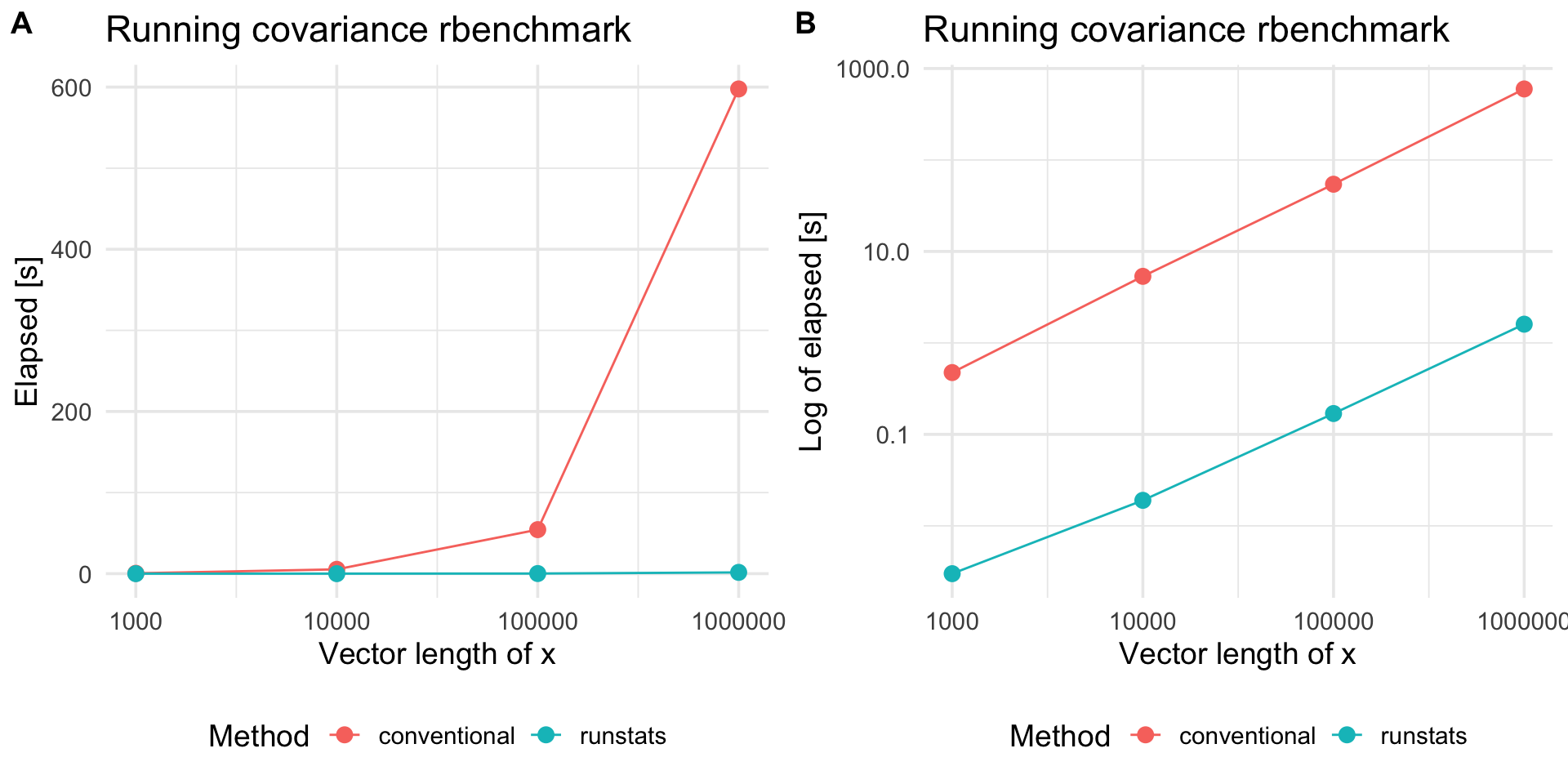

To compare RunStats performance with “conventional”

loop-based way of computing running covariance in R, we use

rbenchmark package to measure elapsed time of

RunStats::RunningCov and running covariance implemented

with sapply loop, for different lengths of time-series

x and fixed length of the shorter time-series

y.

## Conventional approach

RunningCov.sapply <- function(x, y){

l_x <- length(x)

l_y <- length(y)

sapply(1:(l_x - l_y + 1), function(i){

cov(x[i:(i+l_y-1)], y)

})

}

set.seed (20181010)

out.df2 <- data.frame()

for (x.tmp in x.list[c(1,2,3,4)]){

out.df.tmp <- benchmark("conventional" = RunningCov.sapply(x.tmp, y),

"runstats" = runstats::RunningCov(x.tmp, y),

replications = 10,

columns = c("test", "replications", "elapsed",

"relative", "user.self", "sys.self"))

out.df.tmp$x_length <- length(x.tmp)

out.df2 <- rbind(out.df2, out.df.tmp)

}Benchmark results

library(ggplot2)

plt1 <-

ggplot(out.df2, aes(x = x_length, y = elapsed, color = test)) +

geom_line() + geom_point(size = 3) + scale_x_log10() +

theme_minimal(base_size = 14) +

labs(x = "Vector length of x",

y = "Elapsed [s]", color = "Method",

title = "Running covariance rbenchmark") +

theme(legend.position = "bottom")

plt2 <-

plt1 +

scale_y_log10() +

labs(y = "Log of elapsed [s]")

cowplot::plot_grid(plt1, plt2, nrow = 1, labels = c('A', 'B'))

Platform information

sessioninfo::platform_info()

#> setting value

#> version R version 3.5.2 (2018-12-20)

#> os macOS Mojave 10.14.2

#> system x86_64, darwin15.6.0

#> ui X11

#> language (EN)

#> collate en_US.UTF-8

#> ctype en_US.UTF-8

#> tz America/New_York

#> date 2019-11-14